IN THIS EDITION |

||

|

||

|

||

|

||

Growth of India’s gross domestic product (GDP - at constant 2011-12 prices) and gross value added (GVA) at basic prices in YoY terms has been estimated by the Central Statistics Office (CSO) at 5.7% (a 13-quarter low) and 5.6%, respectively, in Q1 FY2018, undershooting expectations. A back-ended pickup in spending by the state governments, the boost from restocking after the Goods and Services Tax (GST), and a favourable base effect would support GDP growth in the remainder of this fiscal. However, the uneven monsoon rainfall over the last six weeks and the year-on-year (YoY) decline in sowing of several crops has clouded the outlook for agricultural growth and rural demand to some extent. Based on this, the low visibility of an imminent revival in investment activity, as well as the subdued Q1 FY2018 readings, we have revised our FY2018 GDP growth projection downward by 30 basis points, to 6.8% from 7.1%. We also discuss the Hybrid Annuity Model (HAM) which has emerged as the preferred mode of awarding road projects by the NHAI, with the awards through this route going up to around 53% of the total in FY2017 from a low 8% in FY2016. Interest from participants has been mixed, with all HAM projects awarded at a premium during February-March, 2017. However, some projects have not been able to achieve financial closure and we examine some of the concerns that lenders still have in this regard. I hope you will find this newsletter useful and informative. Best Regards Anjan Ghosh |

||

In this edition of ICRA Insight, we discuss the performance of the Indian corporate sector and the overall economic growth in Q1 FY2018. The financial performance of the Indian corporate sector slipped during Q1 FY2018, largely impacted by the GST rollout from July 2017. Many consumer-oriented sectors faced inventory de-stocking and offered discounts to clear the pre-GST inventories. In addition, recovery in raw material prices, especially metals, also led to earnings contraction in a few industries. In particular, the growth in aggregate revenues of 448 companies slowed down to 5.3% during Q1 FY2018 from 8.3% in Q4 FY2017, when performance had showed signs of a recovery, post demonetisation. The EBITDA margins fell by 180 bps to 15.7% on a year-on-year (YoY) basis, and were the lowest in the past several quarters.

In this edition of ICRA Insight, we discuss the performance of the Indian corporate sector and the overall economic growth in Q1 FY2018. The financial performance of the Indian corporate sector slipped during Q1 FY2018, largely impacted by the GST rollout from July 2017. Many consumer-oriented sectors faced inventory de-stocking and offered discounts to clear the pre-GST inventories. In addition, recovery in raw material prices, especially metals, also led to earnings contraction in a few industries. In particular, the growth in aggregate revenues of 448 companies slowed down to 5.3% during Q1 FY2018 from 8.3% in Q4 FY2017, when performance had showed signs of a recovery, post demonetisation. The EBITDA margins fell by 180 bps to 15.7% on a year-on-year (YoY) basis, and were the lowest in the past several quarters.

The financial performance of the Indian corporate sector (ICRA’s sample of 448 companies) slipped during the first quarter of FY2018, largely impacted by the Goods & Services Tax (GST) rollout from July 2017. Many consumer-oriented sectors faced inventory de-stocking and offered discounts to clear pre-GST inventories. In addition, recovery in raw material prices, especially metals and rubber, also led to earnings contraction in a few industries.

The financial performance of the Indian corporate sector (ICRA’s sample of 448 companies) slipped during the first quarter of FY2018, largely impacted by the Goods & Services Tax (GST) rollout from July 2017. Many consumer-oriented sectors faced inventory de-stocking and offered discounts to clear pre-GST inventories. In addition, recovery in raw material prices, especially metals and rubber, also led to earnings contraction in a few industries.

The growth in aggregate revenues of 448 companies slowed down to 5.3% during Q1 FY2018 compared to 8.3% in the preceding quarter, Q4 FY2017, when performance had showed signs of recovery, post demonetisation. The EBITDA margins fell by 180 bps to 15.7% on a YoY basis and were the lowest in the past several quarters. Out of the 30 sectors, 17 witnessed contraction in EBITDA margins during Q1 FY2018. Margin contraction was the highest in Telecom, Tyres, Pharmaceuticals, Automobile OEMs, Shipping, Chemicals and Consumer Durables industries. As for the Interest Coverage Ratio (ICR), it stood at 3.5x (adjusted for relatively strong credit profile sectors). While aggregate ICR weakened marginally, sectors with higher level of stress witnessed a stable trend in ICR.

In the automobile sector, sales of the two-wheeler segment grew by 8% as OEMs ramped up production of BS-IV variants and healthy demand from the wedding season in North India. However, the Commercial Vehicle segment sales declined by 9%, primarily due to a sharp contraction in the M&HCV segment. This was because of a deferment by fleet operators ahead of the GST rollout and adverse impact of pre-buying in the previous quarter.

Consumer Durables too witnessed lower sales, impacted by de-stocking even as primary sales remained strong and in fact benefitted from lucrative offers extended by the retailers. Some of the FMCG companies also reported a lower off-take from the institutional segment; especially Canteen Stores Department (CSD), where the impacted was quite significant.

Pharma too was hampered by the GST roll-out, the sector’s Q1 FY2018 secondary sales grew by 7.6%, which was lower than the previous three quarters. After de-stocking in May and June, industry sales contracted in July-17 (down 2.4%) on account of operational issues, related to upgradation of software by wholesalers, which constrained billing to a large extent. The primary sales by companies were even weaker, with reported decline being in high single digit to double digit.

Cement production fell by 3% in Q1 FY2018, impacted first by demonetisation in H2 FY2017 and then by the GST. In addition, sand shortage in North India and drought in Tamil Nadu played spoilsport, demand in eastern region was well supported from retail housing and infrastructure. Despite weak volume growth, cement companies reported stable financial performance driven by sharp increase in realisations, especially in the northern and eastern markets, even as pet coke prices and freight costs increased.

Steel companies’ consumption grew by 5%, reflecting an improvement over the preceding quarter. Growth was driven by healthy demand from the automotive sectors and some recovery from the capital goods segment; as well as a ramp-up in production at new Greenfield units of some of the leading players. Though the high indebtedness in the steel sector continues to remain an overall credit concern, the performance of steel companies was a mixed bag during the quarter.

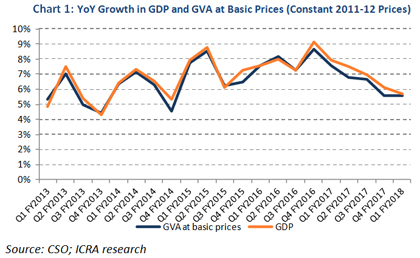

Growth of India’s gross domestic product (GDP - at constant 2011-12 prices) and gross value added (GVA) at basic prices in year-on-year (YoY) terms has been estimated by the Central Statistics Office (CSO) at 5.7% (a 13-quarter low) and 5.6%, respectively, in Q1 FY2018, substantially undershooting our and consensus expectations.

Growth of India’s gross domestic product (GDP - at constant 2011-12 prices) and gross value added (GVA) at basic prices in year-on-year (YoY) terms has been estimated by the Central Statistics Office (CSO) at 5.7% (a 13-quarter low) and 5.6%, respectively, in Q1 FY2018, substantially undershooting our and consensus expectations.

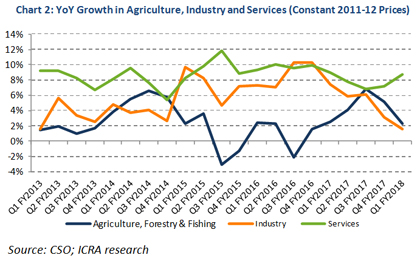

Lower volumes and higher discounts offered to reduce inventories, ahead of the introduction of the goods and services tax (GST), and the turnaround in the average WPI inflation, dampened manufacturing GVA growth to a 20 quarter-low 1.2% in Q1 FY2018. In contrast, trade, hotels, transport, communication and services related to broadcasting recorded a robust 11.1% expansion in Q1 FY2018, mirroring the transient discount-induced uptick in sales ahead of the GST, and improvement in indicators such as rail freight, air cargo freight, fuel consumption etc.

Lower volumes and higher discounts offered to reduce inventories, ahead of the introduction of the goods and services tax (GST), and the turnaround in the average WPI inflation, dampened manufacturing GVA growth to a 20 quarter-low 1.2% in Q1 FY2018. In contrast, trade, hotels, transport, communication and services related to broadcasting recorded a robust 11.1% expansion in Q1 FY2018, mirroring the transient discount-induced uptick in sales ahead of the GST, and improvement in indicators such as rail freight, air cargo freight, fuel consumption etc.

Looking ahead, the uneven spread of monsoon rainfall, both the deficit in several sub-divisions as well as the floods in some of the states, poses a concern over agricultural output and incomes in Q2 FY2018 and Q3 FY2018. Nevertheless, a rise in minimum support prices for various crops, automatic stabilisers such as the rural employment guarantee scheme and crop loan waivers announced by some state governments, would bolster rural consumption. Urban sentiment and consumption demand are likely to benefit from the staggered pay revision for state government employees and pensioners, expected to be announced by several state governments over the next two years. However, pay revision and loan waivers would reduce the fiscal space available for infrastructure spending, since state governments have the leeway to alter a fairly limited set of revenue streams after the transition to the GST. Additionally, the front-loading of spending by the Government of India in Q1 FY2018 may affect the pace of growth in the subsequent quarters.

We expect a moderate upswing in volume growth and capacity utilisation in Q2 FY2018, led by restocking of inventory closer to normal levels. In contrast, the up-fronting of purchases by consumers to take advantage of the discounts offered in the run-up to the GST to reduce inventories, are likely to result in a dip in consumption growth in the subsequent quarters, particularly during the festive season.

We expect a moderate upswing in volume growth and capacity utilisation in Q2 FY2018, led by restocking of inventory closer to normal levels. In contrast, the up-fronting of purchases by consumers to take advantage of the discounts offered in the run-up to the GST to reduce inventories, are likely to result in a dip in consumption growth in the subsequent quarters, particularly during the festive season.

Overall, growth in FY2018 is expected to remain domestic consumption-driven, with a moderate rise in export volumes and aggregate Government consumption. A revival in private sector investments is likely only after the capacity utilisation has risen to healthier levels, businesses have successfully navigated the transition to the GST, and twin balance sheet concerns have eased appreciably. A back-ended pickup in spending by the state governments, restocking post-GST, and a favourable base effect are likely to contribute to higher GDP and GVA growth in the remaining quarters of FY2018, relative to the subdued performance in Q1 FY2018. However, based on the unfavourable trend in kharif sowing, the low visibility of an imminent revival in investment activity, as well as the subdued Q1 FY2018 readings, we have revised our FY2018 GDP growth projection downward to 6.8% from 7.1%.

The Hybrid Annuity Model (HAM) has become the most preferred mode of awarding projects by the NHAI with around 53% of the awards in FY2017 done through this route, compared to 8% in FY2016. Till March 2017 a total of 43 projects, covering 2,641 km, were awarded through the HAM (34 in FY2017 and nine in Q4 FY2016) route garnered a favourable response from both the EPC and the BOT players with intense competition till January, 2017. This is likely to increase in FY2018.

The Hybrid Annuity Model (HAM) has become the most preferred mode of awarding projects by the NHAI with around 53% of the awards in FY2017 done through this route, compared to 8% in FY2016. Till March 2017 a total of 43 projects, covering 2,641 km, were awarded through the HAM (34 in FY2017 and nine in Q4 FY2016) route garnered a favourable response from both the EPC and the BOT players with intense competition till January, 2017. This is likely to increase in FY2018.

On the other hand, almost 67% of the HAM projects till January 2017 were quoted at a discount to the base price, with some being awarded for as low as 65-71% of NHAI’s bid project cost (BPC). The number of bidders for these projects ranged between three to ten. The bid competitive intensity however eased during February-March, 2017 with all projects awarded at a premium during this period. The initial six months post HAM’s launch attracted relatively low participants with aggressive bids - 70% of total awards were at a discount. Subsequently, bidders increased with some moderation in aggression; between July, 2016-January, 2017, there was a good mix of premium and discounted bids with 43% of awards at a discount. It was during February-March, 2017 that a turnaround in trend was witnessed and all HAM projects were awarded at a premium during this period.

The engineering, procurement and construction (EPC) mode continues to remain extremely competitive with a large number of bidders quoting at a substantial discount to the NHAI’s base price, followed by BOT (HAM) projects (moderate competitive intensity) and BOT (Toll) with the lowest competitive intensity. At the aggregate level, the top five bidders won 22 projects, totaling around 1,367 km (52%), for an awarded cost of Rs.203.80 billion (4% discount) to the NHAI's base cost of Rs.212.88 billion.

Given the several inefficiencies that characterize the Indian road sector, lenders’ confidence levels were lowest during HAM launch. Therefore although the letter of awards (LoAs) was signed in January, 2016, the first financial closure under HAM model was achieved only in September, 2016.

As the equity requirement for HAM is low, lenders doubt developers’ commitment till the end of the concession period, given majority developers limited experience in development space. Assuming the debt-to-equity ratio of 75:25, the developer’s equity requirement is just 15% of the total project cost as 40% of the cost is reimbursed by the NHAI during the construction phase itself. In case EPC works are executed in-house, the net equity adjusted for EPC profits is even lower, resulting in developer’s low interest. As a result, three HAM projects have been cancelled till date as developers’ failed to achieve financial closure within stipulated timelines.

The growth in the loan against property (LAP) portfolio of major financiers was the lowest in a decade at 17% in FY2017, down from 40% and 30% in FY2015 and FY2016 respectively. Total disbursements fell, post demonetisation, and as a result remained flat in FY2017, compared to the previous years (increase by 36% in FY2016 and 43% in FY2015). In addition, the declining lending spreads due to increased competition and falling interest rates, worry financiers.

The growth in the loan against property (LAP) portfolio of major financiers was the lowest in a decade at 17% in FY2017, down from 40% and 30% in FY2015 and FY2016 respectively. Total disbursements fell, post demonetisation, and as a result remained flat in FY2017, compared to the previous years (increase by 36% in FY2016 and 43% in FY2015). In addition, the declining lending spreads due to increased competition and falling interest rates, worry financiers.

As for the asset quality, there was a slight deterioration with the 90+ days past due and 180+ days past due loans increasing marginally, the same stood at 2.4% in March 2017 (2.0% in March 2016) and 1.9% respectively (1.6% in March 2016). The annualised prepayment rate in LAP portfolio decreased from a peak level of 34% p.a. in Q3 FY2012 to around 13% p.a. in Q4 FY2017. This implies that lenders are increasingly unable to offer attractive rates for the balance transfer, courtesy the already competitive rates on existing loans. The other key contributing factor is the drop in the share of loans sourced by Direct Sales Agents (DSAs), who often encourage their clients to opt for a fresh loan of higher amount in lieu of the existing loan, after every few years. This apart the stagnant property prices have also played its part.

The LTVs of the LAP portfolios are slowly inching upwards, with average LTV increasing from 40% in FY2009 to 47% in FY2017. Tenures are also moving upwards while ticket sizes are reducing, the latter implying that many lenders are focusing more on Tier II & Tier III locations.

The lenders’ portfolio is concentrated in the top three states - Maharashtra, Delhi and Gujarat (total around 45% of the overall disbursements) and the top 10 cities (total around 57% of overall disbursement). However, lenders are increasingly focusing on Tier 2 cities and their portfolios are steadily getting geographically diversified.

Loans against residential properties continue to form a dominant part of the lenders’ portfolio (56% share), followed by loans against commercial properties (37% share), mixed usage properties (3.5% share) and industrial properties (3.5% share).

ICRA’s study of collection behaviour in its rated securitisation transactions backed by the LAP loan showed a median monthly collection efficiency to be within 95%-100%, indicating a minimal impact of demonetisation.

LAP, as a product, is relatively new hence delinquency for this asset class is unlikely to increase by more than 50-100 bps from the current levels, by March 2018, unless there is a severe external shock. The GST impact on micro, small and medium enterprise (MSME) borrowers will differ sector-wise. Pressures of conforming to the GST norms will mean a systemic disruption in business, and uncertainty around business continuity itself. It will impact borrowers’ loan repayment capacity and may increase delinquencies in the near to medium term. In the long term, however, entities that manage interim challenges and adapt their businesses accordingly will survive and become stronger in the market place. They will also reap the benefits of the GST - reduced tax burdens, improved logistics, faster delivery of services and the elimination of the distinction between goods and services.

| m Rating Updates for the month of August 2017 | |

| Upcoming Events | |

| September 2017: Indian Iron and Steel Sector – Trends and Outlook | |

| September 2017: Indian Retail NBFCs – Trends and Outlook | |

| ICRA in News | |

|

|

Mint – September 18, 2017: The impact of stricter loan defaults discloser norms |

|

Hindu Business Line – September 17, 2017: Bidding guidelines will improve bankability of solar PPAs: ICRA |

|

Economic Times -September 14, 2017 : Monetisation of 75 projects via TOT to fetch Rs 35,600cr: ICRA |

|

Business Standard- September 14, 2017: Logistics sector heads towards evolutionary phase: ICRA |

|

| Contact Us | |

For any queries related to this issue of ICRA Insight, get in touch with

Ms. Naznin Prodhani

naznin.prodhani@icraindia.com

or +91 124 4545860/ 9594929632

Follow us on

HelpDesk +91-124-3341580

© 2017 ICRA Limited. All Rights Reserved ICRA INSIGHT DOES NOT CONSTITUTE OR PROVIDE INVESTMENT OR FINANCIAL ADVICE, NOR DOES IT PROVIDE RECOMMENDATIONS TO PURCHASE, SELL, OR HOLD PARTICULAR SECURITIES. ICRA INSIGHT DOES NOT COMMENT ON THE SUITABILITY OF AN INVESTMENT FOR ANY PARTICULAR INVESTOR. ICRA INSIGHT IS ISSUED WITH THE EXPECTATION AND UNDERSTANDING THAT EACH INVESTOR WILL, WITH DUE CARE, MAKE ITS OWN STUDY AND EVALUATION OF EACH SECURITY THAT IS UNDER CONSIDERATION FOR PURCHASE, HOLDING, OR SALE. IF IN DOUBT YOU SHOULD CONTACT YOUR FINANCIAL OR OTHER PROFESSIONAL ADVISER. ALL INFORMATION CONTAINED HEREIN IS PROTECTED BY LAW, INCLUDING BUT NOT LIMITED TO, COPYRIGHT LAW, AND NONE OF SUCH INFORMATION MAY BE COPIED OR OTHERWISE REPRODUCED, REPACKAGED, FURTHER TRANSMITTED, TRANSFERRED, DISSEMINATED, REDISTRIBUTED OR RESOLD, OR STORED FOR SUBSEQUENT USE FOR ANY SUCH PURPOSE, IN WHOLE OR IN PART, IN ANY FORM OR MANNER OR BY ANY MEANS WHATSOEVER, BY ANY PERSON WITHOUT ICRA’S PRIOR WRITTEN CONSENT. To the extent permitted by law, ICRA and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability: I. to any person or entity for any indirect, special, consequential, or incidental losses or damages whatsoever arising from or in connection with the information contained herein or the use of or inability to use any such information. NO WARRANTY, EXPRESS OR IMPLIED, AS TO THE ACCURACY, TIMELINESS, COMPLETENESS, MERCHANTABILITY OR FITNESS FOR ANY PARTICULAR PURPOSE OF ANY SUCH INFORMATION IS GIVEN OR MADE BY ICRA IN ANY FORM OR MANNER WHATSOEVER. |